⚡️ AR7: A Decisive Turn for UK Offshore Wind

What a landmark morning for the Offshore Wind sector! AR7 is a win—and it’s exactly the momentum the industry needed. ☕️⚡️

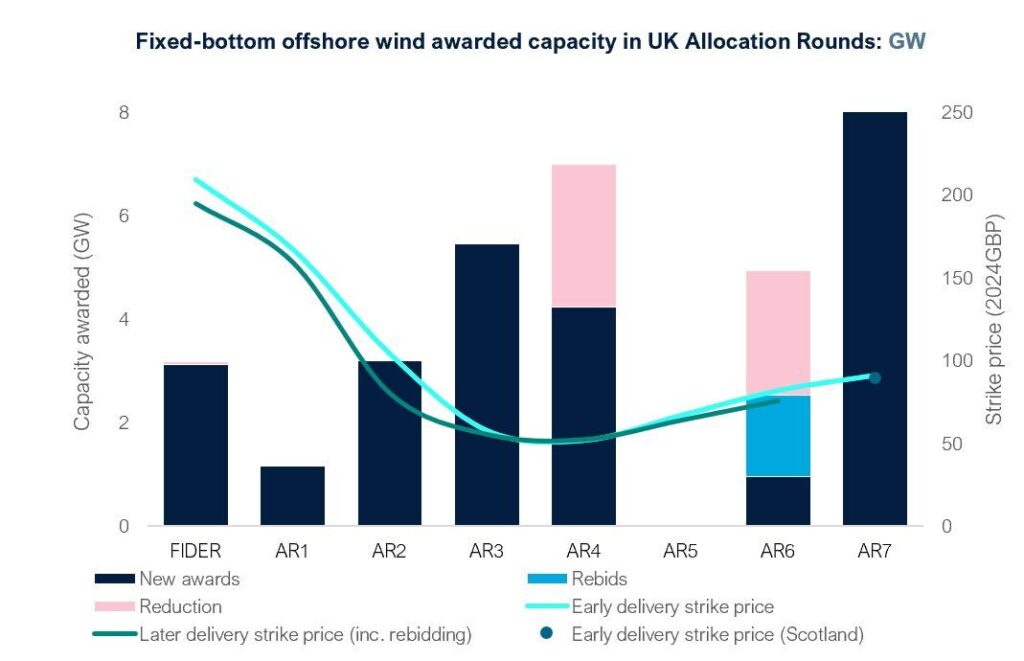

With 8.4 GW successfully back on the board, the UK has sent a clear signal to the global market. We would like to extend a huge congratulations to the winners who are driving this transition forward.

🏗️ Fixed Offshore Wind Awards

6 projects | 8.25 GW | Avg. Strike Price: £91.20/MWh (2024 prices)

Norfolk Vanguard West: 1,545 MW

Awel y Môr: 775 MW

Berwick Bank B: 1,380 MW (£89.40/MWh)

Dogger Bank South East: 1,500 MW

Dogger Bank South West: 1,500 MW

Norfolk Vanguard East: 1,545 MW

🌊 Floating Offshore Wind Awards: 2 projects | 192.5 MW | Avg. Strike Price: £216.49/MWh (2024 prices)

- Erebus: 100 MW (A major milestone for Blue Gem Wind and the Celtic Sea pipeline)

- Pentland: 92.5 MW

🔍 What AR7 Really Tells Us

- The UK is Investable: When contract structures account for the real-world realities of inflation, interest rates, and supply chain pressures, the capital follows.

- Bankability is Back: We are already seeing strategic moves in the capital stack, such as RWE’s success being followed by KKR’s 50% stake acquisition in Norfolk Vanguard.

- The Pipeline is Substantial: These aren’t just headlines—they are “real” anchors for the economy. For example, Berwick Bank has consent for up to 4.1 GW, and Dogger Bank South represents a massive JV (RWE + Masdar) over 100km offshore.

⚠️ The Challenges Ahead

While we celebrate today, AR7 does not magically fix the structural hurdles:

- Grid Reality: Connections and constraints remain the primary bottleneck.

- Execution Capacity: Ports, vessels, foundations, and cables are the next major hurdles.

- Floating Scale: While projects like Pentland and Erebus provide vital momentum, scaling this technology requires a focused financing and skills playbook.

💡 The RECA Insight

AR7 isn’t just a win for the balance sheets; it’s a massive “Green Light” for the UK’s energy transition. With over 8GW back on the board, the industry has proven its resilience. However, an award is only the beginning.

At RECA, we see this 8.4GW pipeline as a call to action. The momentum is back—now we must ensure the technical expertise and supply chain readiness are there to meet it. We are committed to bridging the skills gap, providing the insights and excellence needed to move these projects from “Awarded” to “Operational.”